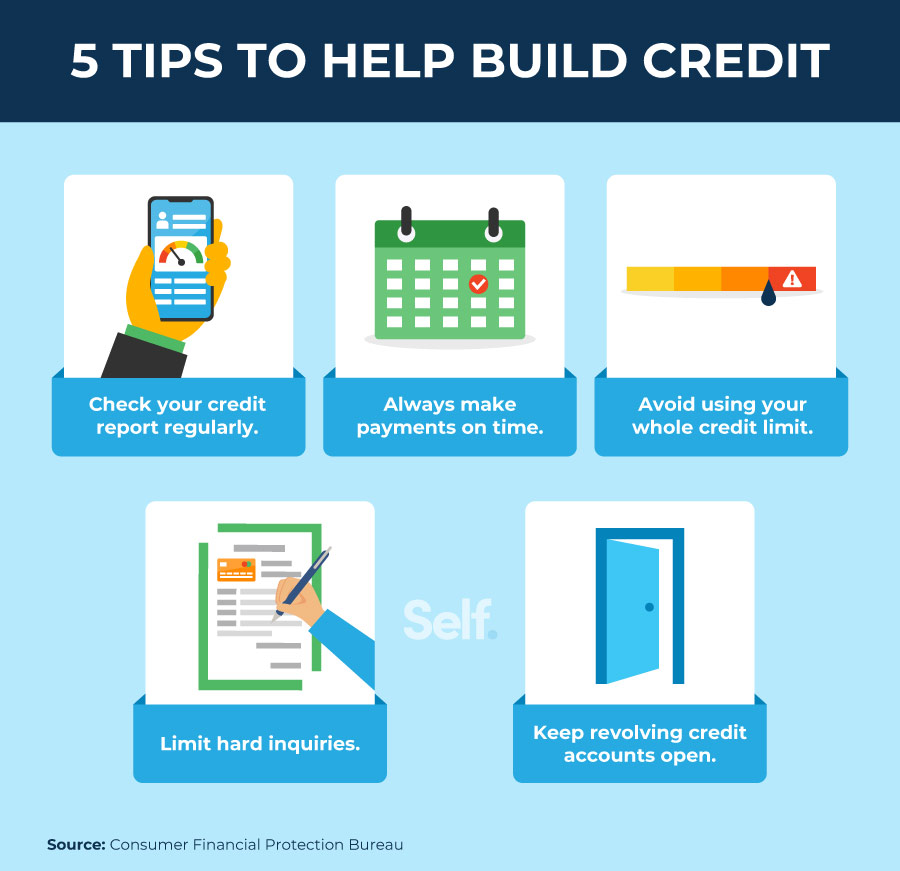

- Review your credit reports having problems: You are entitled from the government legislation to track down a free of charge content of your own statement out of each one of the around three major consumer credit bureaus thru AnnualCreditReport. I encourage closely reviewing all the about three of your credit reports in order to see if there was erroneous recommendations that could be injuring their score, including a belated percentage you made timely otherwise good past-due membership you never ever open. Try to do this early which means you have time to disagreement and right mistakes before you apply to possess a home loan. Otherwise, which have open disputes might complicate the borrowed funds recognition.

- Make any costs timely: The percentage records the most important scoring circumstances, and while making towards the-go out costs will help their borrowing from the bank. Even though an account does not statement their on-day costs on the credit agencies, you don’t want to fall behind and have the membership delivered so you’re able to choices for the reason that it you are going to nevertheless harm the fico scores.

- Do not submit an application for new borrowing from the bank: Starting this new borrowing profile is going to be necessary for financing sales and you may building credit finally. But you fundamentally would not want taking right out financing otherwise beginning handmade cards right before making an application for a mortgage because the app and the membership you certainly will harm your fico scores.

- Pay down mastercard stability: Your own borrowing card’s claimed balance prior to its borrowing limit-its borrowing from the bank utilization ratio-shall be a significant rating factor. While carrying balance, attempt to pay them down as fast as possible to boost your own credit ratings. Even although you shell out the costs completely each month, paying off the bill up until the avoid of each statement period might result regarding the issuer revealing a lowered harmony, which results in a lowered use rate.

- Keep usage price more 0%: Regardless if highest borrowing from the bank usage rates are generally even worse for the credit score, which have a application rates from the lower solitary digits could actually be much better than just 0%. You can do this by paying on the equilibrium until the statement big date and purchasing it well adopting the report shuts and you can through to the expenses flow from. Usually do not rotate credit card stability every month when you can afford to pay the expenses entirely-there’s absolutely no a lot more advantage to your own borrowing from the bank to achieve that and you will you’ll be able to basically sustain expensive desire costs.

The fresh takeaway

It can be you’ll to track down recognized to possess a home loan with a get only five hundred, but that’s that have specific caveats-that you will be applying for an FHA financial and you renders about a good ten% downpayment, to name a couple huge ones.

If you do not already have expert borrowing from the bank, attempting to improve your borrowing from the bank you’ll improve odds of taking accepted and-perhaps researching a diminished rate of interest than your if you don’t manage

Remember that mortgage brokers often fool around with particular credit rating designs when looking at programs. Nonetheless they have differing minimum credit score requirements based on the type of financing, your general creditworthiness, while the details of the purchase. If you want to check the results a lending company is likely to rely on, your https://availableloan.net/installment-loans-ms/ best bet is probably to invest in a registration as a result of myFICO. During that it composing, it works $ monthly.

The financing results you should check free of charge basically are not this new of those you to mortgage lenders fool around with, but may be helpful in giving you an atmosphere where you happen to be at. And many score providers will offer wisdom to the what’s helping otherwise hurting your own get.

Lenders often briefly provide the Classic Credit ratings in addition to the newer results when such alter start. Upcoming, by 4th one-fourth out of 2025, new Antique Results could well be phased out. You will find still particular lingering discussions in the details, but lenders and additionally might have the option of having fun with information and you may results away from a few credit file in lieu of about three.